by James Corbett

corbettreport.com

March 31, 2018

It has been promised for 25 years. Its coming has been heralded as a world-changing event. It has launched a thousand headlines in the last few months. And it happened this week. But if you blinked you would have missed it.

What am I talking about? Why, the launch of a Chinese yuan-denominated oil futures contracts on the Shanghai International Energy Exchange, of course! Or, in more headline-appropriate terms: The Birth of the Petroyuan!

Considering this event has been in the works for literally a quarter of a century (since the Chinese tried and failed to launch such a contract in 1993), the event came and went with remarkably little fanfare, even from the ChiCom mouthpiece press. Take Xinhua's decidedly low-key announcement: "China launches crude oil futures trading." No celebration of the glorious arrival of the dawn of a new monetary order. No bold proclamations about the impending dominance of the Chinese benchmark in global oil sales. Not even a screed about how the fearless leader, President For Life Xi, is bravely steering the country toward a petroyuan utopia. Just:

China on Monday launched trading of the yuan-denominated crude oil futures contracts at the Shanghai International Energy Exchange, which is the first futures listed on China's mainland to overseas investors.

The listed futures for trading are contracts to be delivered from September this year to March 2019. The benchmark prices of 15 contracts were set at 416 yuan (65.8 U.S. dollars), 388 yuan and 375 yuan per barrel, varied by delivery dates.

Li Qiang, Shanghai's Party chief, and Liu Shiyu, chairman of China Securities Regulatory Commission, together rang the gong to open the trading session.

Oh, and the name of this earth-shaking, world-changing futures contract? "SC1809." It's like they're going out of their way to make this as unremarkable as possible.

But still, here it is. The event that everyone's been waiting for. A first, tentative step toward the petroyuan and one potential way for the international community to step away from the petrodollar. So what does it mean?

Well, that really depends whether you're talking short-term or long-term.

I've discussed the long-term ramifications of this move before, most notably in "China’s New World Order: Gold-backed oil benchmark on the way." Quick recap: The Shanghai Energy Exchange's yuan-denominated oil contracts, combined with the Shanghai Gold Exchange's yuan-denominated gold fix means that it may one day be possible for a country (like, oh, say, Russia) to sell oil to China in yuan and exchange that yuan for gold, thus completely bypassing the dollar.

Cue the "end of the dollar paradigm" theme here.

But hold on just a minute. That certainly is the long-term vision that is being pursued here, and there's no doubt that China, Russia, Iran and many other countries around the world would jump at the chance to create a viable alternative to the petrodollar...but are we really that close? Short answer: No. No, we aren't.

Longer answer: Remember when China promised to build an alternative to the SWIFT Network that the banks use to transmit transaction data between countries? You know, the one that's "totally not political" even though the EU strong-armed it into de-listing Iranian banks for political reasons in 2012? And then remember how it emerged that China's so-called SWIFT "alternative" was actually going to be run on the SWIFT Network itself?

Do you think there might be some similar shenanigans going on with this petrodollar "alternative?" If so, then might I just say you are an extremely jaded and skeptical person. You are also correct, so give yourself a cookie.

Just read the fine print on the SC1809 contracts, as related by Xinhua: "At the beginning, US dollars can be used as deposit and for settlement. In the future, more currencies will be used as deposit." So (for the moment, at least) this isn't a golden ticket for bypassing the dollar. Overseas traders will still be putting dollars in and getting dollars out. The yuan will just be the denomination of the contract.

Also, the prospect of SC1809 challenging Brent Crude or WTI for the title of "global oil benchmark" is still a long ways off. China's capital controls and pegging of the yuan mean that it is still useless as a world reserve currency or an international settlement currency. Until Beijing releases its death grip on the yuan, it's not going to be embraced by China's foreign trading partners, let alone non-Chinese trading partners elsewhere in the world.

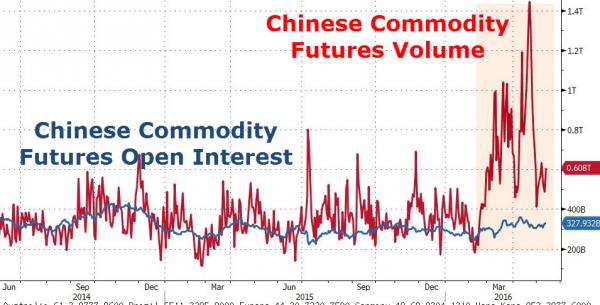

Another factor: China's commodities markets are no stranger to the same speculative frenzy that have led to the highly-risky, highly-leveraged “umbrella trusts” and “Wealth Management Products” and stock-collateralized loans of the Chinese stock bubble and bust. When nickel debuted on the Shanghai exchange in 2015, trading volume surpassed that of the benchmark future on the London Metal Exchange within six weeks. But that volume was part of a general speculative madness. Most Chinese trading steel rebar futures, for example, had no idea what they were trading; they just saw it as another investment opportunity.

So it is not difficult to imagine a similar frenzy happening with yuan-denominated oil futures. It's just another chance for the big returns that Chinese investors have come to expect from the rigged-i-est of the world's rigged markets (to coin a phrase). If such a frenzy does eventuate, though, those investors may want to take note of what happened in China's commodities futures market in 2016. When things got too hot, the Chinese government stepped in to tighten regulations, restrict trading hours and boost fees. In the oil futures space, too, the government can and will intervene whenever they don't like the direction of the market.

Having said all of that, make no mistake: the long-term trend, should it be allowed to continue, is toward the rise of the petroyuan. Consider:

- China is now the world's largest oil importer.

- China has a bid in to buy a 5% stake in Saudi Aramco, and Beijing has been openly courting Riyadh with its Belt and Road Initiative.

- State-owned oil and gas giant PetroChina is buying up companies all along the Belt and Road path, preparing for the Chinese-dominated global trading future.

All of these developments point the way toward a future where China and its trading relationships tip the scale away from the petrodollar and toward the petroyuan. Assuming Beijing does loosen the reins and allow liberalization of the yuan, it will eventually make more sense for nations to settle their bilateral trade with China in yuan directly rather than going through the dollar.

Of course, this all depends on these trends being allowed to continue, which is still an open question. After all, we know what happens to nations that try to step out from under the petrodollar umbrella.

At any rate, don't look for the world to change overnight. But historians of a future era may just be recording March 26, 2018 as the day the change started.